2021 Dual-Use Report

A 2021 study on dual-use tech companies that have successfully raised over $5M of investor funding and comparisons with the 2020 study.

2021 Dual-Use Report

Chase Contreras, Zack Horovitz, Bryan Holst, Richard Tippitt, Ryan Chen

Introduction

AIN Ventures aims to be a leader within the dual-use technology space through diligent monitoring, analysis, reporting, and participation in the investment landscape.

2020 Recap

Last year, AIN published its first dual-use report, predicated on a core assertion that governments will continue to inject capital into dual-use technology investments to concurrently bolster their countries' economies and advance national security capabilities. Our initial research, comprising 500 U.S. companies that have raised over $5M of venture capital, highlighted the following investment metrics: location; industry sector; founder demographics; funding sources (dilutive and non-dilutive); companies' operational status; and their predominant acquisition pathways.

Based on our findings, we concluded the following:

- California, particularly the San Francisco Bay area, and New York remain the predominant headquarters locations for entrepreneurs. However, smaller, more affordable, pro-business cities like Austin, TX, have boomed in popularity and are attracting young tech talent away from Silicon Valley. The resulting talent migration and demographic shift are creating innovation hubs across the country.

- Cybersecurity startups lead the way. Specifically, Defense and Administrative tech attracted the predominance of capital investment within the dual-use ecosystem. Large, bureaucratic organizations continue to have an appetite for IT and other support services that improve internal operations and security. Due to restrictive entry barriers and challenging market conditions, other dual-use areas like Space and Health Tech experienced less investment activity.

- Founder demographics had wide bounds, but the top of the bell curve was predictable; mostly Caucasian males in their late 20s/early 30s with Google/Harvard MBA resumes. Diversity, including representation by veteran founders, remains disappointingly low. Founding teams typically ranged between 1 and 3 people with technical backgrounds.

- Just over a third of companies in the sample received funding under SBIR/STTR, showing strong growth in support of non-traditional startups. Plug and Play, Techstars, and Y Combinator led the accelerator programs. In addition, new Enterprise Associates, In-Q-Tel, Alumni Ventures Group, Andreesen Horowitz, and Sequoia made frequent top-five appearances on capitalization tables and continue to assert a dominating presence in the Venture Capital arena.

- Most companies in our sample are still privately owned. In terms of acquirers, there is no clear trend. A few legacy technology companies have acquired multiple dual-use startups on our list, but most acquirers only make a single appearance. Of our 500-company sample, 137 companies have been acquired compared to just 33 that have gone public, meaning an acquisition is a 4x more likely exit strategy than an IPO for dual-use tech companies.

Now on to 2021 - Our Methodology

To generate our database for 2021, we utilized Crunchbase to screen for companies that met the following criteria during the 2021 calendar year:

- Dual-use technology: both commercial and government (not necessarily military) applications

- Raised at least USD $5M in investment funds

- Founded after the year 2000

- Still operational or acquired

- Headquartered in North America or Western Europe

We generated an initial list of 2000+ companies, filtering for all the criteria above except for Dual-use, which is not a common database capability. We then examined each of the companies in the initial list, taking out those that did not meet our standard for dual-use until we were left with 188 in our final sample. Finally, from the shortened list of company names, we created our database by pulling data on these select companies from a single source (Crunchbase) and verifying information when possible from Pitchbook. In addition, we filled in missing information, such as founder demographics and accelerator history, through LinkedIn and manual searches.

It is essential to acknowledge that in our initial data collection, we concentrated our efforts on companies that explicitly market themselves as dual-use technologies or have technologies that have clear use cases applicable to both commercial and government markets. As a result, it is possible our database does not adequately capture companies with technologies that the government could potentially use but for which the government is not their primary focus (e.g., health tech). Furthermore, our initial data pull had a prominent representation of Biotech companies in 2021. However, these were mainly therapeutic or pharmaceutical companies, with only a few being relevant for government use when taking a closer look.

Headquarters Locations

Dual-use Startup Locations: Rise of Dual-use tech in Seattle, Denver, and LA

Overall the HQ Location of the dual-use startups has primarily remained the same from 2020. The Bay Area region continues to lead the way for HQ cities, with New York and Austin also having a notable presence of dual-use startups. However, there was a greater than 2.5x increase in companies out of Seattle, Denver, and LA in 2021, matching the reporting seen throughout 2021 detailing these cities' fast growth in the tech landscape.

2021 HQ Cities Increase from last year's data: 3 Growing Dual-use Tech Cities

2021 HQ State and Regions: California leads the way, again.

Key Industries

Broad industries: Agencies require back-office assistance

Our analysis divided dual-use technology companies into seven primary categories, shown in the chart above. Similar to our 2020 findings, AdminTech, i.e., IT and other back-office services that improve the government's internal operations, dominate the dual-use space, but these technologies have been matched by a rapid rise in funding of Defense Tech. Defense Tech is an umbrella term that encompasses dozens of "stovepipes" ranging from IoT to VR. Still, most of the companies that fit our sample for 2021 were some flavor of cybersecurity and/or AI. The market is flourishing, and due to the numerous ways AI can be applied, companies within the AI subsegment can consistently raise capital. In future reports, we believe that it may make sense to analyze the AI industry related to dual-use on its own.

Specific industries: The growing importance of data

Artificial Intelligence (AI) based companies experienced a significant uptick in capital flow while VC funding to the cybersecurity industry continued its meteoric growth. The rise in AI start-ups in the dual-use space could potentially be attributed to advancements in technology and the announcement of huge deals in the industry globally. While AI increased in popularity in 2021, cybersecurity maintained the lion's share of the dual-use industry start-ups. The continued growth of these industries year-over-year stems from the "Great Power Competition" and Washington's increased emphasis on innovation to ensure we do not fall behind our competitors. We will address this in more depth later in this year's Dual-use Tech report.

Other Company Details

Founding dates: Growth in dual-use over time

Dual-use tech companies appear to follow the same development trajectory as other startups. After the dot-com crash, we see a gradual increase in the number of dual-use companies founded. However, the numbers taper off as we approach the present day because companies typically take 3-4 years to raise the $5M required to meet our analysis threshold.

Technology type: Software leads

Software remained at the top business type to succeed in the dual-use tech space, unlike hardware that larger, more established companies dominate.

Founding team size: Small teams

Similar to 2020, 2-3 person founding teams are most common, accounting for nearly 75% of the 188 companies reviewed for this paper. Many assumptions can be drawn from this, but founding team membership is a poor metric for projecting the success of a start up due to the fluid nature of these teams. Founding team members can easily and discreetly be added (or, less often, removed), and though the dynamic at the company may change, the performance should remain consistent. Again, these numbers are merely a snapshot in time and will be valuable in assessing a single company's progress year-over-year, but not the entire industry.

Startup experience: Prior startup experience is not essential

Mirroring our 2020 dataset, most founders in our sample do not have previous startup experience. While experience certainly helps in dual-use startups, it is not a barrier to success.

Government experience: No advantage

Similar trends were seen in 2021 regarding founder government experience, indicating that government experience is certainly not necessary for successful dual-use startups.

Past employment: No clear pattern

In this year's review, one clear conclusion is drawn - tech founders come from tech companies. The top nine most recent employers from this year's study account for almost 20% of founders' previous employment. This conclusion departs from earlier findings, which indicated that large tech companies were not the "hubs of innovation" they claimed to be. On the contrary, the founders of growing tech businesses are made in the ranks of giants like Microsoft, Google, Oracle, Uber, and Facebook.

Age of founders: Consistent with other studies

The median of our age data for founders is 32. We observed a pattern of founders launching their startups upon completion of graduate school. We also saw a spike in 40-50-year-old founders.

Diversity: Improvement in Founder Diversity

Regarding inclusion and diversity, minority representation in the dual-use space has shown improvement with a greater than 20% increase in companies that have some diversity in their founding team. However, this remains significantly higher than the average seen across all startups having some founder diversity, estimated at 23% by the World Economic Forum.

Our 2021 sample contains increases across all underestimated racial minority groups: Black founders increased to over 4% across the sample size; Hispanic founders by around one percentage point; Asian founders jumped to over 26%; and Middle Eastern/Others climbed to nearly 18% of founders. This is a boon for the dual-use tech sector as more diversity undeniably means better products, greater inclusion, and increased ability to assess talent in the industry.

Degree types: Technical backgrounds

99% of founders in the 2021 sample have an undergraduate degree. In addition, three of four have technical backgrounds (science and engineering degrees in that category), demonstrating the importance of a founder's hard skills in the dual-use tech start arena.

Continuing the trend from 2020, only 47% of dual-use founders do not have a graduate degree, and only about 3% of founders have a Ph.D. Advanced technical degrees and MBA's were the most popular education routes among those with postgraduate degrees.

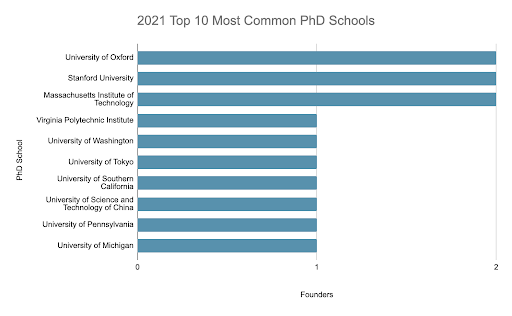

Schools: More Representation from International and State Schools

While Stanford and Harvard remained at the top of the list in 2021, there was a surprising uptick in founders from international institutions and state universities. The majority of the international founders attended Indian and Israeli schools before founding companies in the US. These companies were heavily weighted toward SaaS and AI industries. Additionally, the University of Illinois Urbana-Champaign and Utah State had solid undergraduate representation among founders.

Technical degrees contributed the most to the graduate school line-up, with strong engineering programs being the common denominator.

Most PhDs in our sample were in technical degrees, with 30% of the founders with PhDs attaining them from foreign universities. This data point may represent the disparity in the importance of doctoral degrees in the US compared to other countries.

Investors and Accelerators

Government grants: Not required for success

Only about 10% of companies in the sample received funding under SBIR/STTR. This alone cannot be used to assess the importance of government grants on innovation, and this data is subject to the same fluidity as some of the other data points collected here as this is merely a snapshot of one portion of an industry. However, in the past 12 months, a few key laws have been brought before Congress - and some passed - that lower the barriers to government funding and incentivize tech companies to access government funding to grow their business. This is the heart of dual-use technology and signals a shift back to a healthy and robust relationship between the public sector and private industry.

Most common investors: Insight Partners play a huge role in dual-use tech development

2021 dual-use funding was almost completely supported by venture capital. Major firms led most funding rounds and familiar names - Insight Partners, Sequoia, Lightspeed, Dell, and Andreesen Horovitz (A16Z) - dominated the top 10, with those four firms funding nearly 25% of all companies in our study. This continuing expansion of venture capital funding is consistent with the increase of software companies dominating the tech space. Software companies neatly fit the profile of an excellent venture capital investment due to their scalability and likelihood of exit in a relatively short (7-10 years) amount of time.

Accelerators: No real surprises

The most well-renowned accelerators in US venture capital again topped this list, with Y Combinator and Techstars backed companies leading the way.

Operational status: Mostly private companies

Only three of the companies in the year's data are public. Some conclusions could be drawn from this, but what is most important to keep in mind is that the maturation process of a tech company does not necessarily have a linear path. These companies may experience rapid, exponential growth one year and, in the next year, plateau while growing the business internally or completing an aggressive R&D process. Alternatively, it may not be beneficial or desirable for these companies to IPO - case in point: SpaceX, which remains private despite being the most visible and one of the most successful commercial space companies in the Space Tech ecosystem (and contracts with the government).

Like IPOs, the number of acquisitions in a given year does not necessarily convey anything novel - in our 2021 data, only three of the companies reviewed had been acquired. However, with the number of young tech companies creating novel products in the dual-use space, especially in the AI industry, it is possible that in the next two to three years we will see large successful exits via acquisition of many of the companies that were reviewed this year.

Why Dual-Use: A Brief Analysis of "Great Power Competition"

Great Power Competition is an umbrella term that defines the diplomatic and economic relationship between major world powers, namely the United States and the People's Republic of China (PRC). For the past two decades, the PRC, through the Chinese Communist Party (CCP), has aligned its instruments of national power to support rapid economic growth and the adoption of new technologies. In recent years, this rapid expansion has been used to grow their military, expand their borders, and cast a shadow on their neighbors and also the US's regional partners. This integration of military power, economic dominance, and expansionist ideas make China the US's most significant competitor. It is an excellent case study in understanding the power of dual-use tech in the future geopolitical landscape.

Fifty years ago, when President Nixon visited China, its economy was less than 10% the size of the US economy. In the ensuing decades, China has bloomed into an economic powerhouse through a well-known program of copycat innovation. However, that innovation is useless without China's true advantage: a vast captive user base. Chinese "innovation" is a single source for the nearly 1.5 billion person country. The rapid expansion of Chinese technological prowess is primarily because adoption happens on such a large scale.

This process of iterative development and advancement has spread across all industries. Coupled with the PRC's Military Civil Fusion (MCF) program, China can scale the technological advance of its military at a pace almost unbeatable by any other competitor on the planet. The MCF program uses both legitimate and illicit means to further the national security goals of the PRC and CCP. The ambitions of the PRC are well known as they continue to expand and infringe on sovereign territory in the South China Sea and threaten Taiwan.

In the US, where the independent (from government) technological advancement and adaptation process is respected, the Senate passed the Innovation and Competition Act of 2021 on 8 Jun 2021, and the bill passed in the House on 4 Feb 2022. This bill can be seen as a counter to the MCF program, where the US government has formalized and endorsed the processes by which scientific research, innovation, and adoption occur. Additionally, this bill supports those individuals and organizations dedicated to these processes.

This and previous endorsements by the US government of technological innovation and advancement have flung open the door for dual-use tech. We expect to see the field of software-as-a-service (SaaS) grow the most, with the need for cybersecurity being the most pressing priority. In a close second will be space tech. Space tech is subdivided into dozens of verticals, but maintaining relevance in the great power competition will come down to placing critical satellite assets in orbit and securing their communications, specifically those related to position, navigation, and timing. Finally, following space tech, defense tech, in general, will see significant growth as weapons systems become more automated and networked, reducing the risk and the cost of using human operators.

Applicability: Analysis of geopolitical landscape in eastern Europe

The AIN Team is composed exclusively of current and former military officers, and it's an important characteristic of our unique value proposition. Our core team and syndicate, with their backgrounds across all five service branches, have a unique insight into the applicability of dual-use technologies since we have been end-users of this equipment or services.

Further, our team sees the value in specific dual-use technologies in these complicated geopolitical times. To demonstrate this, we examined the current crisis in Ukraine following the unprovoked and unlawful invasion by Russia in late February 2022. We believe this crisis will spur a surge of dual-use tech, specifically in cyber security, artificial intelligence (AI), space tech, financial, and disaster preparedness/response tech.

The first and most significant employment of dual-use tech was the widely reported deployment of SpaceX's Starlink satellite internet service. After massive cyber attacks by the Russian government, much of Ukraine was left without reliable internet service. Following a request on Twitter, SpaceX deployed hundreds of ground terminals to access the constellation of nearly 1,500 low-earth orbit internet satellites to restore connectivity to those living and fighting on the ground in Ukraine. As a result, Starlink is now providing the essential internet connectivity service to those in need to support rescue and evacuation operations. This highlights the rapidly expanding importance of commercial space launches.

AI is a booming tech across several verticals and is critical in the information war in Ukraine. The Russian army is leveraging AI in the form of autonomous weaponry; however, the extent and effectiveness of these weapons cannot be determined. AI is being employed in the defense of Ukraine to stem the impact of disinformation campaigns coming from Russia. Unverified reporting is rampant on both sides of the conflict, and tech giants like Twitter, Meta, and Telegram use AI to sift and prevent misinformation from reaching the public domain. This tech is being scaled to support strategic state objectives and more tactical needs.

The care and evacuation of non-combatants are always complicated but have been especially tough in Ukraine due to limited infrastructure and non-resilient telcom. We forecast that disaster technology will be another segment of dual-use tech that will expand due to this ongoing crisis. Along with the COVID pandemic, global attitudes towards inventory/preparation have shifted from "just-in-time" to "just-in-case," with governments at all levels willing to spend extra capital on materials and services that safeguard their citizens and increase their resilience in the face of possible disasters. The invasion of Ukraine has demonstrated the need for resilient public services, the organization of critical supplies, and a network of disaster response professionals who can support the public in times of crisis.

Russia was hacked on March 4, 2022 by the "hacktivist" group Anonymous. The group successfully hacked into Russia's television network and displayed footage of Russia's bombing campaign against Ukraine. Before the hack, Russian civilians were under the impression Putin was successfully operating a non-violent military operation. A decentralized hack of this magnitude highlights vulnerabilities for all state players. As a result, Cyber Security platforms are more crucial than ever. As a result, we will likely see a massive increase in development and innovation in this space.

Shortly after the invasion of Ukraine, seven major Russian banks were taken off of the ubiquitous Society for Worldwide Interbank Financial Telecommunication (SWIFT) system, cutting them off from critical time-sensitive information and dealing a severe blow to Russian financial integrity. This, coupled with sweeping sanctions from the international community, has had devastating impacts on the overall Russian economy and Russian citizens. In response to these actions, there has been space created for innovation of financial tech, spinning off cyber security, in order to safeguard both personal and state assets. Russia is also adopting lesser-known alternatives, namely from their partner China, to stay afloat in these uncertain economic times.

Government Marketplace

As discussed in last year's report, government funding plays an essential role in catalyzing innovation. The U.S Government has recognized the asymmetric investment returns of dual-use technology and has played a more significant role in the dual-use space. As a result, we've seen a significant increase in the DoD's allocation of non-dilutive capital over the last decade. The chart below demonstrates the $163B increase in the Pentagon's spend on contracting efforts since 2017. The trending increase represents roughly a 10% CAGR.

We witnessed a continued capital allocation to the U.S. Government's primary small business investment vehicles: the Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR). The SBIR and STTR programs are highly competitive contract opportunities that encourage domestic small businesses to engage in Federal Research and Development (R&D) with the potential for commercialization. SBIR is a multi-phase Government-sponsored incubator that aims to innovate technologies that address critical American priorities (defense, bolstering the economy, sustainability, etc.).

Based on the available data, there was only a minor increase in total dollars obligated for STTR/SBIR programs between 2020 and 2021. Additionally, there was a 10% decrease in total contracts awarded in 2021.

The graph above shows total obligations have fluctuated significantly over the past ten years. Fluctuation can be attributed to a confluence of factors; political volatility/turnover in administrations, overall economic health, budget constraints, etc.

As demonstrated below, the predominance of SBIR/STTR funding in 2021 is allocated to the Department of Defense (DoD), followed by the Department of Health and Human Services (HHS).

Because the awarding of SBIR funding, particularly Phase I and II funding, occurs so early in a company's development cycle, we view SBIR funding as a leading indicator of where innovation is happening. Considering this, California seems to have a bright future in the dual-use tech space. The Golden State was the top location for companies successfully winning SBIR/STTR contracts. We provided the slide below to show that Menlo Park, the San Francisco Bay Area, and Los Angeles prove to be competitive cities in the startup ecosystem for 2021.

AIN Ventures is bullish on the SBIR/STTR program and supports the concept. However, we recognize a significant flaw – many of these Government "seed" companies will fall trapped in a purgatory state known as the Valley of Death. The Valley of Death occurs when a DoD-funded, or heavily government-focused startup, fails to scale and achieve wide commercial adoption. Unfortunately, the traditional government acquisitions process, and even many innovative bypasses to the federal acquisitions regulation (FAR), fail to move at the speed necessary to prove a product's viability before many companies need to raise capital. This process hurts startups in two ways. First, they cannot raise enough non-dilutive funding to sustain operations, especially if building bespoke iterations of their commercial product for government customers. Second, their focus on the government hinders their ability to show traction and subsequently attract commercial funding. As a result, institutional investors without this understanding tend to avoid deals with companies solely or primarily focused on government customers. Investing in such technology requires patience and tenacity with which most investors are uncomfortable.

AIN Ventures' unique value proposition to our limited partners and prospective portfolio companies is that we are all veterans with an acute understanding of the Government marketplace. Additionally, we have strong entrepreneurial and early-stage investing experience. As a result, AIN will leverage its expertise and connections to identify strong, overlooked startups that need assistance with concurrently managing DoD and commercial marketplace expectations. In 2021, AIN Ventures monitored the Government startup landscape and zeroed in on several targets.

The United States Innovation and Competition Act in 2021 was a major triumph for America's dual-use ecosystem. This $250 billion bill is a 5-year spend plan designed to boost the United States' technological competitiveness with China, specifically targeting semiconductor production, scientific research, artificial intelligence, robotics, biotechnology, and space exploration. A significant catalyst for this bill is the U.S.'s inability to sufficiently source computer chips. Seventy-five percent of the world's chips today come from Asia, while the share of semiconductors manufactured in the United States has fallen from 37% in 1990 to 12% today. In addition, global supply chain shortages during the pandemic highlighted massive vulnerabilities to our infrastructure; entire sectors of the US economy abruptly stopped due to over-reliance on certain imports.

Beyond investments in scientific research and development, the bill includes various national security measures designed to thwart cyberattacks, foreign infiltration of domestic supply chains, and exfiltration of U.S. intellectual property, with a particular focus on threats from China. This bill is not only a win for the US, but it also improves the viability of AIN Venture's thesis.

The US Government's demand for technology innovation will continue to increase throughout 2022. Even before Russia invaded Ukraine, Washington passed the National Defense Authorization Act signaling an increase in SBIR funding. We predict that growth will likely continue due to both geopolitical events and the clear policy changes that further incentivize technology innovation for government use.

Another legislative initiative stoking the flames of innovation and technological advancement is President Biden's Infrastructure Bill. Baked into this $1T package is a significant allocation for R&D spend. In addition, President Biden's bill will draw talent and institutional capital into the dual-use ecosystem like the Innovation and Competition Act.

On the horizon for 2022

Our country faces strong headwinds as we grapple with a tumultuous geopolitical landscape. The Federal Reserve will conduct multiple interest rate hikes to combat inflation. Higher interest rates restrict access to capital and result in lower corporate profits and M&A activity. Rising interest rates and tightening monetary policy will shift the investment landscape and drive a decrease in valuations.

This shift allows younger VC firms with deployable capital to realize stronger equity positions at more advantageous terms. Although macroeconomic trends forecast depressed valuations, we predict the continued injection of raised VC funding into the market will buoy valuations.

As mentioned previously, non-dilutive funding has increased significantly. As a result, the intersection of Dual-Use and DeepTech is AIN Venture's sweet spot - and the time to strike is now. We estimate that there is $30B+ per year in non-dilutive government funding, and the passage of the Innovation and Competition Act will significantly increase this amount. We are confident this funding increase will attract world-class talent, innovation, and investment into the dual-use space, bolstering the viability of AIN's thesis.

In Closing

AIN is enthusiastic about the future of innovation through technology, and our team is confident we will identify the right venture backable companies that positively affect how we live, work, communicate, and play. The combination of in-depth analysis of successful start-up metrics and understanding geopolitical tides is essential for our continued impact.