2024 Dual-Use Report

Our fifth annual Dual-Use Technology report — analyzing 645 DU companies that raised over $5M in 2024, with deep dives into trends, geography, and investment patterns.

By Spencer Read, Andy Coen, Sean Kesluk, Bridgette Simonte and Sherman Williams

Overview

Welcome to our fifth annual Dual-Use (DU) Technology report, where we analyze our internal database of DU companies that have raised over $5 million of Venture Capital funding. We aim to gain insights into trends within the DU landscape by actively monitoring companies within the space.

Background

Venture Capital showed signs of upward momentum in 2024, with total VC investment in the U.S. increasing ~30% over 2023's total to $209.0B. One-third of total capital deployed occurred in Q4, suggesting some dealmaking momentum leading into 2025. Artificial Intelligence (AI) startups captured 60% of this year-end surge (and AI captured 46% of all 2024 VC investments), reinforcing the role of AI as the primary driver of venture activity in 2024. While this year's total dollar amount increased, the number of deals declined, illustrating capital concentration and a lack of capital distribution across a broad set of companies. Mega-rounds of $100M+ accounted for a substantial total of deployed venture funding and 74% of fundraises in Q4 alone. Venture fund formation in the U.S. again failed to reach $100B, as in 2023. However, the likely shift in regulatory posture under the new administration has signaled the prospect of a more lenient and active M&A landscape, forging new optimism for startup exits and a recycling of capital back into the venture ecosystem. Expect to see a continuation of large and AI-driven venture investment in 2025.

Small businesses experienced a surge in optimism in 2024 as inflation concerns eased and consumer spending remained strong. Leading indicators like employment and wage growth improved, and higher interest rates helped cool inflation. However, the overall economic growth forecast was just 2.4%, reflecting the impact of sustained high interest rates, supply chain issues, and tighter labor markets.

DU startups faced unique challenges and opportunities in 2024. While they benefited from government initiatives like the Infrastructure Investment and Jobs Act, the Inflation Reduction Act, and the CHIPS and Science Act, they also navigated the complexities of national security concerns and export controls, influenced by the ongoing conflicts in Ukraine, Gaza, and the Red Sea.

The rise of emerging technologies and geopolitical tensions led to increased scrutiny of DU technologies. Governments prioritized national interests, impacting investment decisions and driving innovation toward regionalization. This shift away from globalization created both challenges and opportunities for DU startups, requiring them to adapt to a new era of national security priorities.

Furthermore, Limited Partner (LP) agreements have historically restricted VC investments in defense-focused DU technologies due to concerns about military-specific applications that involve the loss of human life. However, the increasing strategic importance of DU technologies is gradually shifting this perception and attracting more VC interest. Investors and LPs increasingly realize both the impact and potential wealth-creation opportunities of emerging technologies like AI, Quantum Computing, and Space Technology on both the government and commercial sectors.

Methodology

This year's analysis includes 645 DU companies and 725 unique founders that successfully secured funding in 2024, with a total funding per company amount of $5 million or more. The initial dataset was collected directly from Crunchbase using our proprietary DU criteria and funding filters. This initial list was supplemented with companies that received a Phase II or Phase III SBIR award in calendar year 2024 from the US Navy, US Air Force, and US Space Force, cross-checked with Crunchbase to confirm that these companies have raised greater than $5M in total funding. The combined dataset was then enriched using our APIs to collect founder education and work experience data, U.S. grant data, and U.S. clinical trial data. We note that the accuracy of our data is limited to the accuracy of our data set; therefore, we ask that you focus on the directional nature of our information.

Key Findings

- California, particularly the Bay Area, maintains its prominent position in the DU startup landscape. However, there's a growth in funding distribution across the country compared to previous years. While California continues to lead, Texas, Massachusetts, and New York are emerging as strong contenders in company headquarters.

- Cleantech, aerospace, and advanced manufacturing startups are emerging as pivotal players within the DU technology landscape, showcasing remarkable growth and potential. The AI and machine learning industries continue to assert themselves as major players within the DU startup space. Given expected IRA-related reductions in the new administration, cleantech investments will likely decrease in future years.

- In our analysis of the 2024 data pool, approximately one in five of DU startups were awarded a Small Business Innovation Research (SBIR) status. The strong representation of SBIR-awarded startups underscores the importance of government support in driving innovation and fostering growth within the DU technology landscape.

- The shifting sentiment from SaaS to hardware continues in 2024, fueled by increased investor buy-in and government incentives to solve hard defense and DU problems.

Top HQ Cities

California cities continue to hold a commanding grip on US DU venture capital, with 5 of the top 10 cities accounting for 54.3%. Notably, Texas cities have two entrants, with Austin and Houston making up almost 20% of the top 10 (up from 4.2% last year). With several large defense contractors and energy companies attracting top talent in Houston, and with the city's very own 16-acre innovation hub, Ion District, we can expect Houston to continue to grow into the future. And having earned the nickname of "Silicon Hills," Austin continues to foster a synergistic environment for startups and with AFWERX, the Defense Innovation Unit (DIU), and NavalX having just launched a new Joint Defense Innovation workspace in Austin, DU startups will continue to thrive there.

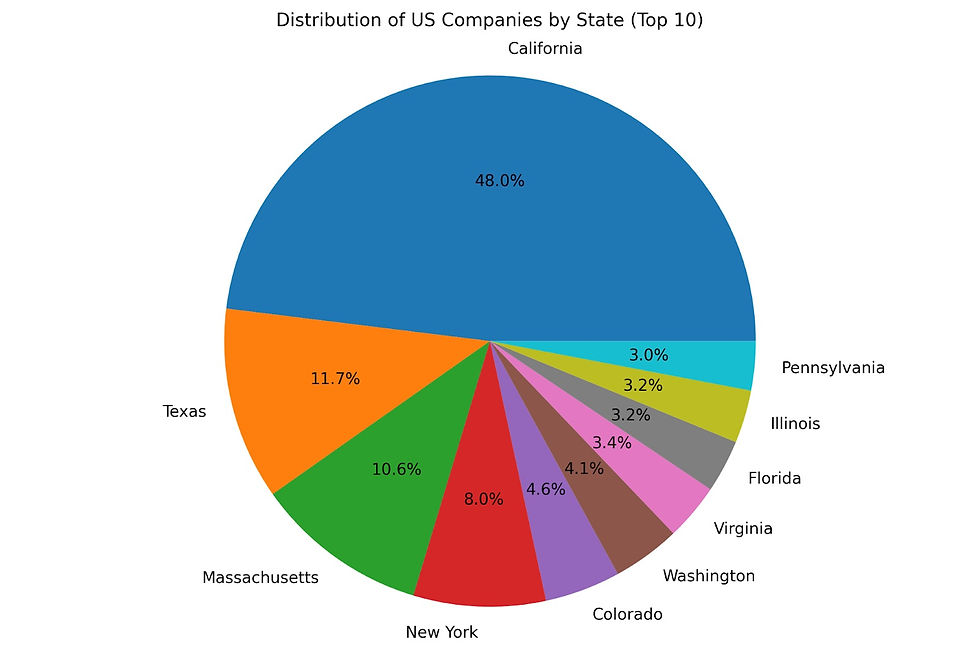

Top HQ States

As expected, the state of California continues to maintain a grip on DU companies. Mirroring top US cities, though, Texas has surged to 11.7% (up from 7.3%), surpassing both Massachusetts and Colorado. While Massachusetts holds a solid third place, Colorado saw a marked decrease from 14.5% in 2023 to 4.6% in 2024. New York also breaks into the top five with 8%, a notable increase from just 1.8% of the share in 2023. Washington and Virginia hold steady, while Florida makes its first appearance in the top 10 and Illinois and Pennsylvania return, knocking out Maryland this year.

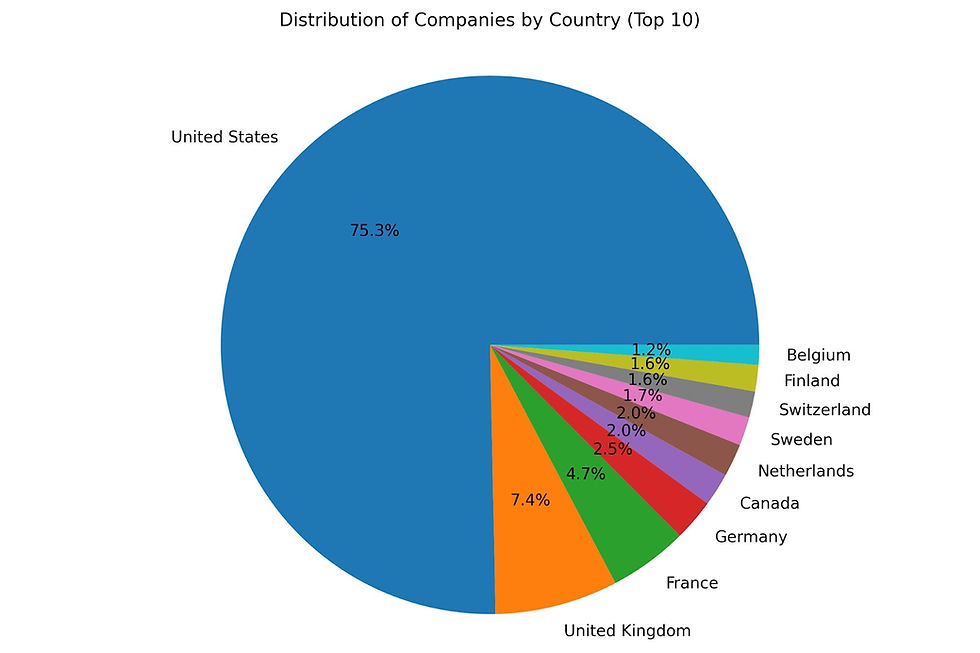

Top HQ Countries

The story told by the data in 2024 was the resurgence of U.S. dominance. The number of DU companies headquartered in the US jumped from just over half in 2023 to three quarters in 2024. Canada declined significantly, while the remaining companies are primarily concentrated in Europe. This may reflect the tapering off of the momentum for capital inflow to European companies in the wake of the war in Ukraine.

Technology Type

Hardware has shown a steady increase from 2021 to 2024 (14% to 37%), while software's contribution has decreased substantially over the same time period (70% to 29%). Hybrid technologies blending hardware and software also increased in 2024. The increasing emphasis on hardware likely reflects a broader market shift and VC buy-in toward hard defense problems, given the geopolitical environment and increasing government incentives to tackle these issues.

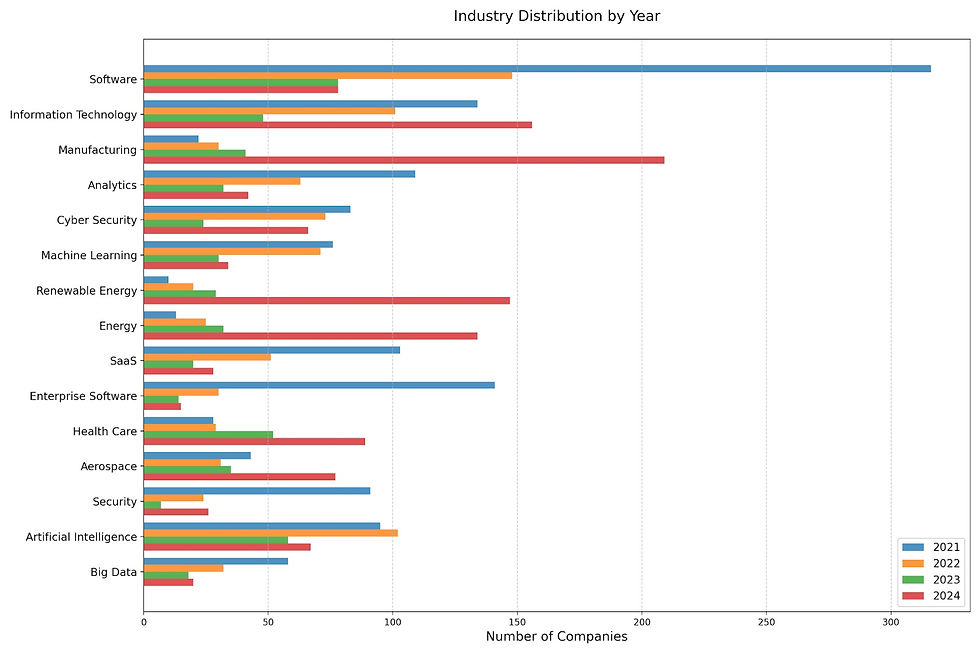

Companies by Industry (2021-2024)

The industry distribution from 2024 reflects the broader trend toward hardware and provides further insight into its drivers. Manufacturing, Renewable Energy, and other Energy DU startups display the highest year-over-year growth in 2024. Software, SaaS, and Enterprise Software have continued their overall decline in representation since 2021.

The rise of AI-powered smart factories that capitalize on additive and 3-D manufacturing in 2024 has reshaped the manufacturing process, contributing to the spike in manufacturing startups in 2024. The efficiencies that robotic and AI-powered manufacturing startups bring to the manufacturing process are proliferating in large organizations as they are acquired. In renewables, energy storage solutions have rocketed in 2024 as solar and wind power technologies mature and the Levelized Cost of Energy (LCOE) improves. The marked shift toward hardware-focused DU startups and away from software, SaaS, and enterprise software demonstrates a willingness to take on what are perceived as the most pressing challenges of the day. As an example, drone warfare in the Russia-Ukraine Crisis, the Red Sea, and the Israel-Hamas war has led to the rise of UAS, counter-UAS, and attritable drone technologies as investors realize the value of unmanned aerial warfare.

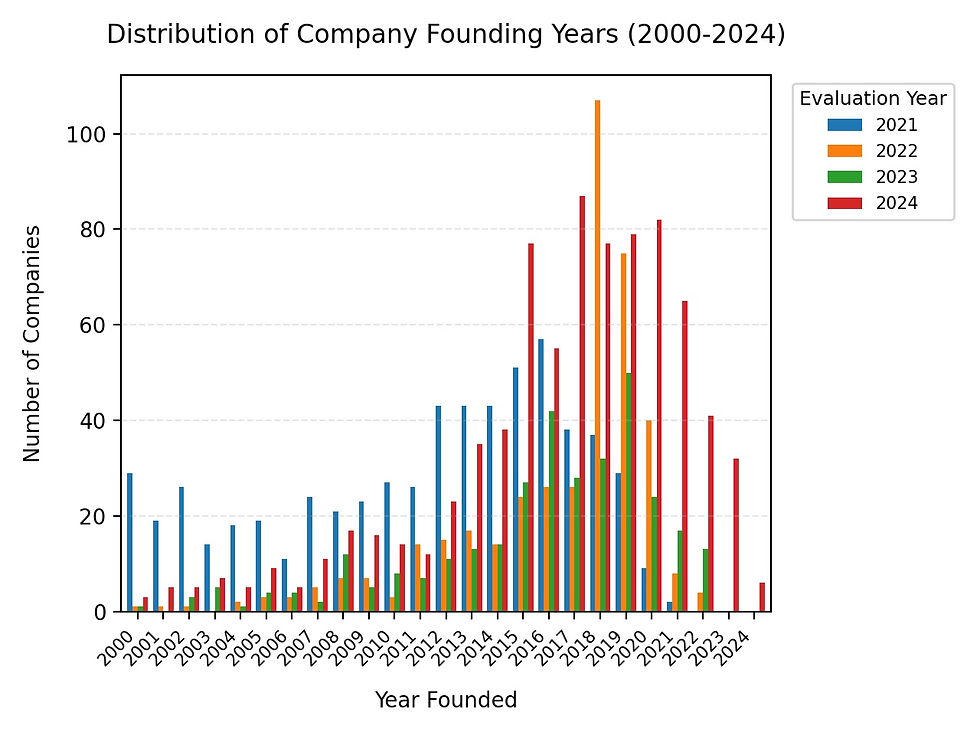

Companies by Year Founded (2021-2024)

The data show a clear concentration of companies founded between 2015 and 2019, with 2018 and 2019 being particularly active years for company formation. A noticeable drop-off in formation emerges after 2020, which may be explained by the challenges of the COVID-19 pandemic and the time required for a company to mature to greater than $5M in funding.

The concentration of $5M funded DU companies in the 6-10 years of age range is indicative of the time it takes for DU companies to mature as they navigate government processes and build strategic relationships for growth.

Number of Founders (2021-2024)

In 2024 and previous years, solo and dual co-founders are the most common trend, accounting for over two-thirds of all companies captured in the data set. Two-person founding teams are the most common, accounting for about 40% of all companies. Large founding teams (5+) are consistently rare across all years.

The DU market requires a focused approach, and smaller, more agile teams are preferable to navigate regulatory complexities. The strong prevalence of dual co-founders suggests the importance of bringing technical and operational expertise from multiple sectors to appeal to government and commercial applications. Additionally, investors might favor smaller founding teams, believing they are more nimble and efficient in navigating the challenges of the DU market.

Previous Employers (2024)

Looking at last year's report, there is a noticeable shift in founders previously employed by universities or university labs (like Lincoln Labs at MIT). This suggests that technical and academic expertise has become increasingly valuable in the formation of a DU company.

The year 2024 previous founder employers saw a cross-section of universities known for their technology prowess, as well as big technology and defense firms. Additionally, 2024 saw a number of new entrants to the Top 10 previous employers, notably MIT and Stanford topping the list, with UC Berkeley the other university within the top ten. The presence of IBM, Microsoft, Google, and SpaceX in the top ten suggests the growing application of commercial technology like AI/ML, robotics, automation, remote sensing, and energy solutions to defense and government. This trend is expected to exponentiate as these sectors mature over the next decade.

Founder Government Experience

In 2024, we see a slight increase in founders with some government agency experience to 6.9%, up from 6.5% in 2023; however, the portion of founders with government backgrounds has remained relatively unchanged. Overall, there has been a slight downward trend in the percentage of founders with previous government experience or military service.

Diversity of Founders (2024)

In 2024, the data shows representation amongst all race and gender categories in DU startups declined. However, unlike previous years, in which data was compiled manually, this year we pulled data directly from Crunchbase without any human enrichment. Given the change in the DEI landscape worldwide, it's reasonable to conclude that the data lacks some accuracy. As such, any wide-sweeping conclusions about diversity representation, given the change in data quality would be ill-founded.

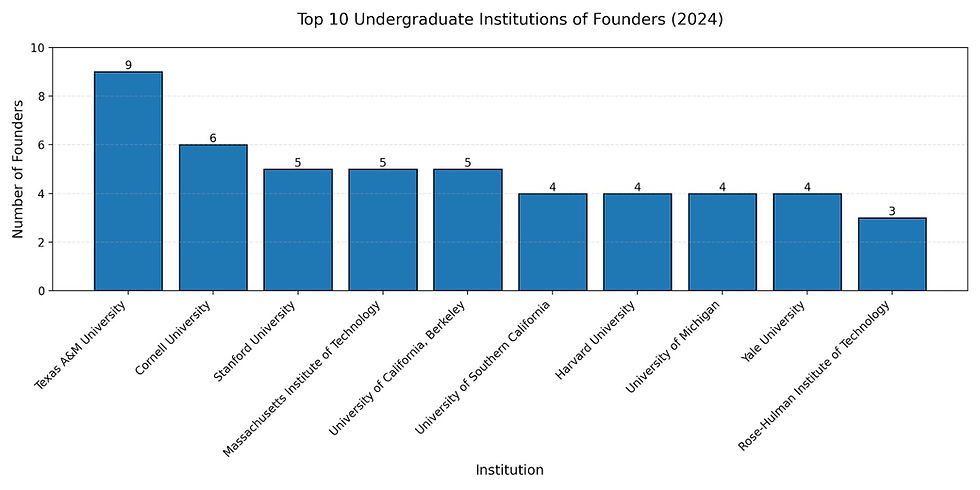

Top Undergraduate Schools (2024)

Similar to previous years, undergraduate institutions do not show a strong correlation to the founding of a DU company. However, with Texas A&M University boasting the single most founders this year and California schools consistently in the top 10, the presence of strong universities in Texas and California yields a synergistic effect with the states' supportive ecosystems and underscores their prominence among DU startups.

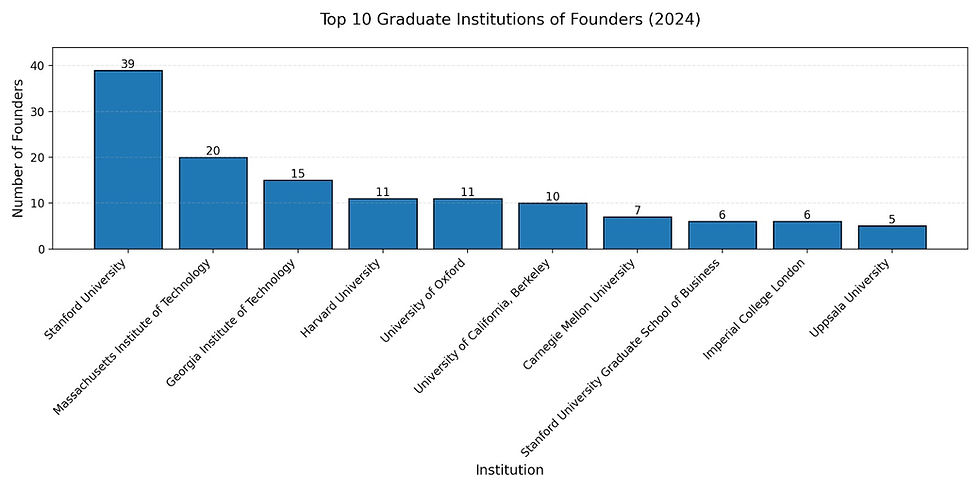

Top Graduate Schools (2024)

In 2024, Stanford and MIT continue to have the strongest representation in graduate degree programs amongst DU founders and the top three institutions, all characterized by strong engineering programs, underscore the growing emphasis of technical expertise in the leaders of this sector. We also see a concentration in foreign countries, namely the UK and Sweden, likely in response to the ongoing Russia-Ukraine conflict.

Graduate Degrees (2024)

In 2024, of the 725 unique founders in this sample size, 50.3% have graduate degrees. Of the graduate degrees obtained, only 3.3% are MBAs, a significant decrease compared to previous years in which MBAs steadily accounted for ~15%. As noted in an earlier chart, with the increase in emphasis on hardware solutions, the technical acumen of founders is increasingly imperative. This is evident in the overwhelming prevalence of founders with degrees in specialized fields.

Top VC Funds (2024)

In 2024, we see a notable increase in the number of venture capital investments across the board. While this does not consider the size of investments, the increase in activity is a promising sign compared to the 2023 data. Alumni Ventures and Khosla Ventures were among the top 6 in 2023 and demonstrated continued interest in DU startups with the most investments in 2024.

Small Business Innovation Research (SBIR) Grant Data

America's Seed Fund is coordinated by the Small Business Administration and funded through 11 participating federal agencies that fund innovations through the Small Business Innovation Research (SBIR) program. These grants provide non-dilutive funding to develop technology and chart a path toward commercialization. While most companies do not have grants, approximately 17.6% of companies in 2024 have at least one. Though this does not consider the check size, this number is up from 14.7% in 2023 and just about at the four-year average of 18% of companies receiving at least one grant. When we examined companies before 2016, we saw a negative correlation between companies raising VC funding and those same companies being SBIR recipients. That began to change after 2016, and the correlation has become stronger over the years.

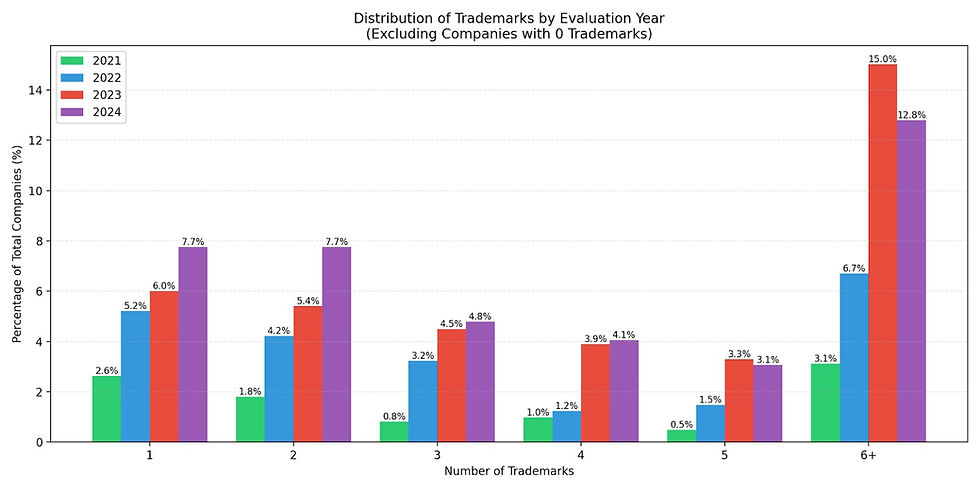

Trademarks Granted

Trademarks reflect protections for brand identifiers that distinguish goods and services. There has been steady growth in companies with 1-2 trademarks across the previous few years. We've also seen a notable increase in 6+ trademark startups since 2021 (3% to 13%). The increasing trademark activity may result from the expansion of the DU and defense technology ecosystem, as well as the growing need for competitive differentiation amongst startups.

Patents Granted (2021-2024)

Companies with 6+ patents represent the largest group amongst patent holders, ranging from 15.9% (2022) to 29.4% (2023) of total companies. This indicates the criticality of protecting intellectual property rights in the DU technology space. It also suggests the positive signaling that patented technologies give to investors.

Single patent holders consistently represent 5.5-7.5% of total companies, and the distribution shows a slight downward trend in mid-range patent holders (2-5 patents). As companies shift to open-source business models, the question arises: Will patents continue to demonstrate technical expertise to investors in the coming years, or will patents be reserved for core innovations to foster collaboration among industry giants? Time will tell, but in 2024, patented technology remained a positive signal for investors.

On the Horizon for 2025 and Early 2026

The interplay of economic factors, geopolitical tensions, and technological advancements characterized the DU startup landscape in the United States in 2024. While startups faced challenges due to the high cost of capital and increased regulatory scrutiny, they also benefited from government initiatives and growing venture capital interest.

The ongoing conflicts worldwide highlighted the importance of DU technologies in modern warfare and national security. They also underscored the need for the responsible development and deployment of these technologies, considering their potential impact on human rights and international security.

Looking ahead to 2025, the DU startup ecosystem is poised for continued growth and evolution. As technology advances and geopolitical tensions evolve, DU startups will play an increasingly critical role in shaping the future of national security and defense innovation. This will be heavily influenced by the DoD budget restructuring in 2025, which remains in flux.

The increasing involvement of venture capital firms and the shift towards private sector-led R&D are accelerating innovation in healthcare, biotechnology, quantum computing, sustainability, space technology, and advanced manufacturing. However, startups must navigate regulatory compliance challenges, funding access, and geopolitical risks to succeed in this dynamic landscape. The trends of 2024 suggest a maturing ecosystem with a greater focus on national security, regional collaboration, and strategic investment. This evolving landscape presents challenges and opportunities for DU startups, requiring them to be agile, adaptable, and resilient to thrive in the years to come.

The DU sector will continue to grow as heightened geopolitical tensions around the globe intensify. The ongoing conflict in Ukraine has caused the US and Europe to re-evaluate the role of rapidly deployable advanced technologies in conflict. The conflict has highlighted the problems with the US government acquisition process, likely prompting the pilot program in the 2024 NDAA to compress its timeline. Ukraine has also highlighted the importance of Unmanned Autonomous Vehicles in modern warfare, as well as a slew of shortcomings with this technology, which the government will rely on the private sector to address. Additionally, continued Russian cyber attacks against Ukraine have showcased the importance of a robust cybersecurity infrastructure, an issue of keen interest to the US and Europe alike. We expect the DU tech ecosystem to continue to garner attention from lawmakers and VC funds and remain less susceptible to fluctuations in volatile markets or broader VC macroeconomic trends.

Healthcare, biotechnology, quantum computing, sustainability, and advanced manufacturing are also considered DU technologies due to their increasing significance in national security. All of these areas were mentioned in the National Standards Strategy for Critical and Emerging Technology, and we believe that increasing investments in these industries will continue. The broad applications of DU technologies allow for some fantastic investment opportunities, although navigating the industry is complex and requires a thorough understanding. AIN aims to assist investors and companies alike and to continue to offer opportunities to invest in this space.