Is Defense Technology in a Bubble?

A quantitative analysis of public comparables and precedent transactions to determine whether Defense Tech is currently in a bubble.

By Sherman Williams, Forrest Underwood, James Palmer, Chris Porter, Cael McCormick, and Derek Reim

We at AIN Ventures have been participating in the Defense Tech sector with a mix of excitement and caution over the last several years. Our excitement is rooted in the fact that as Veterans who run a deep technology fund with a dual-use investment lens, it is encouraging to see storied funds that are enthusiastic about a subsector of dual-use, Defense Tech. An openly competitive geopolitical environment necessitates a strong Defense Tech sector, with part, not all, of that "strong" definition defined by the ability of a country to create new technologies and rapidly put them in the hands of a warfighter. Leveraging all elements of the civilian population/commercial sector to ensure military superiority has been a reality since post-World War II.

"This war (World War II) emphasizes three facts of supreme importance to national security: (1) Powerful new tactics of defense and offense are developed around new weapons created by scientific and engineering research; (2) the competitive time element in developing those weapons and tactics may be decisive; (3) war is increasingly total war, in which the armed services must be supplemented by active participation of every element of civilian population."

A Report to President Truman by Vannevar Bush, Director of the Office of Scientific Research and Development, July 1945

Our caution is rooted in the realities of public company valuations and precedent transactions regarding hardware technologies, which is correlated with Defense Tech. Defense Tech valuation headwinds include customer concentration (only selling to the DoD), long sales cycles, contracting mechanisms that limit upside, low margins of hardware companies, high CapEx necessary to get to commercialization, and regulatory restrictions that potentially limit sales to foreign entities.

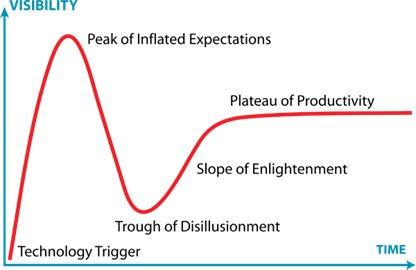

We believe that a balanced approach to Defense Tech investing is imperative. The United States' ability to fight, win, and deter future conflicts means that the formation of an investment bubble in the sector has much greater negative implications than recent technology bubbles (see VR headsets, crypto, micro-mobility, etc.). The health of U.S. security may not be able to handle the lag time as the Defense Tech industry undergoes a hype cycle.

This leads us to ask the question: Are entry valuations of Defense Tech companies justified based on exit possibilities, or in other words, is Defense Tech currently in a bubble?

Indicators of a Bubble

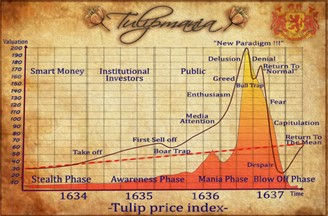

Financial bubbles have occurred since time immemorial and are a standard element of capitalism.

One great example is the Tulip mania that hit the Dutch Republic (now the Netherlands) in the early 17th century and was marked by the astonishing rise and subsequent fall in the prices of tulip bulbs. Economist Charles Kindleberger states that the speculative bubble falls into five phases: displacement, price boom, investor euphoria, profit-taking, and panic. Distinguishing between a legitimate boom and a speculative boom (i.e., bubble) is often difficult to determine until after the fact. Common indicators of a bubble include unsustainable price increases that do not align with their fundamental values, widespread public enthusiasm that's often accompanied by "fear of missing out," which draws in more investors, general market overvaluation, a widening gap between the bubble asset or sector and the broader market, international trade imbalances, and a lower interest rate environment which encourages lending and borrowing.

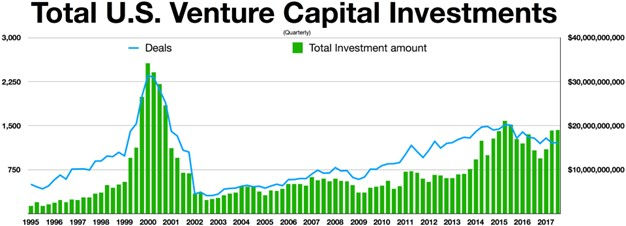

The chart below illustrates VC investment during the dot-com bubble:

Charts: https://www.pwc.com/us/en/technology/moneytree.html

Comparable Companies and Precedent Transactions Analysis

In attempting to answer this question, we conducted a quantitative analysis of public comparable companies and precedent transactions relevant to Defense Tech startups. Given the broad range of domains and technologies that Defense Tech startups encompass - from sea, cyber, and space to hardware, software, and even software-defined hardware - we use several buckets of companies to draw our comparison. Consequently, we focused on six key categories from which we chose our samples to streamline our analysis, as annotated in the tables below. We think this selection is sufficiently broad to confidently answer the question at hand while still being manageable and within the scope of this whitepaper.

Pure Play Defense Tech

These companies are defined by the fact that they mainly sell to the defense sector and are hardware-focused. The majority of this segment is quite mature at this point, as illustrated by their large amount of revenue and low revenue growth. The maturity level of these companies means that they do not necessarily trade on an EV/Rev basis, like most startups that are still in growth (and unprofitable) mode. Still, we do note that revenue multiples are quite low for this group.

Space Companies

Companies were placed in this group because they either have all or at least the preponderance of their revenue in the Space Tech sector. Space Tech is classically representative of dual-use technology, with the majority of revenue for many of these companies likely coming from the defense sector today; however, some of these companies will play a key role in the burgeoning commercial space sector. The public markets have not been favorable to Space Tech companies. We believe that there are private Space Companies that likely have stronger fundamentals than this set, but we have limited information. SpaceX is the superior example of this, with an estimated $13.3B revenue in 2024 and secondary transactions for SpaceX stock going for $200B. These companies are hardware-heavy, which is reflected in their gross margins and revenue multiples. Rocket Lab is a clear outlier, with an 8.14x EV/Rev, likely reflecting that it is currently the best-of-breed public Space Launch company.

Defense Services

These companies operate in both the hardware and software space and provide a range of consultative-like services largely to DoD. Consulting-like services can be labor intensive, and this is reflected in their gross margins, which are low relative to a productized software offering like Palantir, whom we address below. Based on maturity level, these companies largely trade on EBITDA multiples. Revenue multiples for this group are low.

National Security Software

These pure-play software companies sell largely to the U.S. National Security infrastructure and other government entities like law enforcement. It is important to highlight Palantir and its high EV/Rev multiple due to its strong revenue growth and high margins. Please note that the mean and median are the same because only two companies are in this set.

Large Cap GovTech Software

These are primarily software companies (although some have hardware SKUs) that make most of their money outside the government. Each company generates significant revenue from the government. Many of these companies are mature and largely trade on Price/Earnings and Price/Earnings to Growth ratio.

Small Mid-Tech Mid-Cap

These are smaller, primarily software-focused firms that have significant government practices. With a significant portion of revenue coming from software, this group is similar to the Large Cap Govtech Software group with its high gross margins relative to the other comparable groups we examined.

Examination of these defense-focused comparable companies highlights the valuation differences that arise for primary hardware vs. primary software companies, which are reflected in their gross margins. Revenue growth further magnifies the picture of valuations. Defense technology companies that seek to IPO will face the same "market forces" / be seen in the same light as these comparable companies.

Precedent Transactions

An examination of precedent transactions in the defense technology sector reveals relatively high EV/Rev multiples compared to comparable companies. Further, it reveals how acquisitive private equity has been in defense technology. This aligns with past research that AIN has done on niche defense tech sub-sectors like space tech, where you similarly see a high level of private equity activity. In general, an acquisition is more likely than an IPO for defense tech companies, and if an acquisition does occur, private equity is a very likely acquirer. As a general rule, private equity will often bid less to acquire a company than a strategic acquirer.

Our comps and precedents analysis clearly illustrates that companies with strong revenue growth and high margins are rewarded in the market. It also shows that private equity plays a key role in defense tech acquisition, with approximately half of our precedent transactions sample involving private equity. This has implications for the exit potential of defense tech companies.

Role of VC in Defense Tech

Venture capital plays a crucial role in Defense Tech. During the formative years of modern-day venture capital, from the 1950s to the 1970s, investors predominantly focused on hardware technologies. This period saw a surge in investments toward tangible, hardware-based innovations essential for defense, aerospace, and manufacturing. The onset of the personal computer and related software in the 1980s caused a massive shift in VC focus.

Two things are true: i) software-only companies have a higher chance of achieving outsized outcomes, and ii) venture capital has become the leading source of innovation. VC rewards risk-taking allocators backing entrepreneurs that tackle the world's toughest challenges in a for-profit company setting. Increasing geopolitical conflict and a rapidly evolving battlefield are revealing a pretty big challenge, and VCs are doing what they do: they are stepping in to fund companies that are solving key Defense Tech problems.

Warfare is rapidly evolving with the weaponization of artificial intelligence, deployment of unmanned autonomous vehicles, drone advancements, electromagnetic warfare, biotechnology threats, and emerging space technologies (which are often hardware-heavy). The very nature of many of these technologies means that VC-backed companies are well suited to develop them, and the role of VC in ensuring these innovative defense technologies get into the hands of warfighters is becoming more important.

The excitement that we mentioned at the beginning of this article is that the VC community seems to have a great deal of enthusiasm to tackle these Defense Tech challenges. Despite this enthusiasm, we cannot help but notice that the majority of these challenges are hardware in nature. With the exception of infrastructure (see NVIDIA or Broadcom) and energy commodities (see Exxon Mobil), the public markets are currently not rewarding hardware-centric companies, as illustrated in our comps and precedents analysis. Therein lies the dilemma. VC activity in the defense sector will eventually decline without VC-like returns; however, the public markets do not seem to reward defense and defense-associated companies on the same level as other traditional markets where VCs typically invest.

So why is there this enthusiasm if the potential outcomes are likely lower relative to software outcomes? Below, we explore some possibilities.

Modern Warfare = Software + Hardware

A key source of enthusiasm is the increasing role that software plays in military operations. Software enables advancements such as establishing a common operating picture (see Project Maven), as well as other key capabilities such as cybersecurity, DevSecOps, command and control (including autonomous weapons systems), communications, intelligence, surveillance, reconnaissance, and finally embedding advanced software into weapons systems to make them more lethal. The Venture Capital asset class has traditionally supported software innovation, which will likely continue within the DoD.

"The most important six inches on a battlefield is between your ears. Engage your brain before you engage your weapon." — General Jim "Mad Dog" Mattis

While General Mattis' words remain true, autonomy and software-defined weapons systems add nuance to the statement.

Autonomous systems are quickly leading modern combatants down the path of algorithmic warfare. These autonomous systems can rapidly find + fix + finish enemy combatants without human intervention. This rapid processing of information and decision making enables significant tactical and, eventually, strategic advantages. We want to highlight that these unmanned autonomous systems fundamentally change the attack calculus, considering the attacker does not have to worry about loss of life while inflicting maximum loss of life on the enemy. Further, these autonomous systems can be used in situations that are not ideal for humans - from long-duration missions to inherently dangerous missions like operating in a radioactive environment. The VC asset class has a demonstrated ability to field innovative software, and we believe this will continue to be the case with autonomous systems.

Historically, software has been a subordinate element to hardware in weapons systems. That is no longer the case. We have now entered the era of software-defined weapons systems, which are redefining the battlefield. Whether it be a missile system or fighter aircraft like the F-35, a large portion of the functionality of weapons systems actually comes from the hardware. As is the case with autonomous systems, the combatant that is able to employ software that enables them to maximize the capabilities of their hardware will possess a tactical and, eventually, a strategic advantage.

As the need for world-class software in all aspects of military operations increases, the opportunity for defense-focused software companies increases.

Dual-Use Potential

There is the potential that the DoD will fund technologies that will eventually have strong revenue-generating applicability in the commercial sector. To be more clear, a larger slice of the Defense Budget as well as non-budgeted DoD Spend (i.e., Other Contingency Operations, Spending on Ukraine, etc) will go toward dual-use technology startups. AIN Ventures is firmly within this enthusiastic dual-use camp. When we say "fund," it means that the government will provide non-dilutive funding to a company that enables its product to get to market with reduced CapEx spend. The government will also be an initial customer, which helps de-risk a company's ability to make initial commercial sales. The idea is that after proving the product via the government, the company can transition into the commercial market, with much larger revenue potential.

Disruption of Defense Tech Primes

Another potential source of enthusiasm may be the belief that as the DoD seeks to bring innovative technologies to market more rapidly, it will shift some money away from prime contractors toward smaller, more nimble, and ideally more innovative Defense Tech startups.

We must also note that with revenues currently in the hundreds of billions of dollars, there is the prospect of the prime contractors subcontracting under Defense Tech startups to bring the DoD its desired capabilities rapidly. As with anything, relationships matter, and AIN believes Prime Contractor spending on lobbyists provides them with a competitive advantage that will be difficult for Defense Startups to imitate at scale. Further, these Defense Startups, particularly in hardware, may have issues providing the scale that DoD needs, and this is yet another reason to partner with a larger prime. A symbiotic relationship can form where the startups provide the innovation, and the defense primes provide scale and government contracting know-how. Startups at the earliest stages can ally with a Prime, embarking on a "Partner to Win" strategy. Once they demonstrate capability to the government and achieve escape velocity, they can become prime contractors for their specific capability and establish market share.

Lastly, the defense budget is so large that even a 1% shift in current Prime spending towards startups can create numerous defense-focused unicorns.

Large DoD Budget Has Potential to Increase

The DoD accounts for approximately 50% of the discretionary budget in the U.S., reaching $850B in 2023. Increasing geopolitical conflict and rapidly changing battlefields mean that it is highly unlikely that the Defense Budget will decrease any time soon. The Defense Budget is also at an all-time low relative to GDP, meaning it has room to grow based on historical precedence. However, we acknowledge that potential growth is somewhat limited when framed in the context of entitlement spending being much higher relative to the past.

That said, today's tax burden on Americans (and U.S. Corporations) is low relative to other periods in U.S. history when there was intense geopolitical conflict. Last time we checked, the U.S. Government has not lost the ability to increase taxes, and if some of these tense geopolitical situations we have mentioned turn kinetic for the U.S., we may see an increase in taxes. We note that in addition to raising taxes, you could see a cut in entitlement programs, but we assess that cutting entitlement programs is even more untenable than raising taxes.

Balanced View of Defense Tech

While there are several reasons to be optimistic, there are also several reasons to be wary of Defense Tech investing. Some of the key reasons include contracting mechanisms that limit margin upside, customer concentration, and long sales cycles.

While the pool of money available to the DoD is large, it is finite. Within these constraints, government contracting officers are incentivized to acquire the best capability at a low cost. Unlike the commercial sector, brand appeal does not drive up price. Fundamentally, this limits the margin upside for government contracts relative to what can be achieved in the commercial sector. Contracting mechanisms like fixed-priced contracts place an inordinate amount of risk on a company and could easily end in a profit loss for those that sell to U.S. DoD. There are numerous other contracting mechanisms available to the government, but again, the government is incentivized to save money, which limits the upside for vendors. The challenges of contracting mechanisms and customer concentration go hand-in-hand. When companies are building products that will only be used by the government, their pricing/contracting leverage is degraded relative to either a dual-use or purely commercial product that has multiple customers. We acknowledge that there are instances where the government will be willing to pay more than is necessary, particularly if the DoD knows it must keep its vendor in a healthy financial position so that the vendor can continue to recruit the best talent, innovate, and deliver the best product possible. Said another way, the DoD cannot "run its vendors into the ground." It needs to keep them healthy, but our fundamental point is that in the framework of a finite budget and having only one customer, companies have no chance of making a profit, similar to working in the commercial sector.

Lastly, DoD sales cycles can be quite long, particularly for upstart companies. It can take years to earn a place on the Program of Record. This reality is off-putting for a VC-backed startup, particularly when the DoD is the only customer.

Is Defense Tech in a Bubble?

The short answer is it depends. Based on current public company comparables and precedent transactions, current entry valuations are questionable at best and are simply too high at worst. The earliest-stage investors (pre-seed and seed) can deliver venture-like returns, but later-stage investor returns are doubtful based on comps and precedents. This creates an issue because VC-backed companies are uniquely suited to ensure innovative technologies and capabilities are in the hands of warfighters. The landscape could shift in a way that enables exit potentials that would justify higher entry valuations, including i) the increasing importance of software in defense operations benefitting VC-backed startups, ii) investors believing a defense-focused technology will also have dual-use commercial appeal, iii) disruption of defense tech primes, and iv) a rising defense budget.

What is incontrovertible is that the security of the United States cannot afford a deep trough of disillusionment that exists in most hype cycles and the lag time/fall off in investment activity that typically comes with it. A balanced Defense Tech investment sector is a national security issue.

Exhibit 1: Comparable Companies and Precedent Transactions Exhibits

Pure Play Defense Tech

Space Companies

Defense Services

National Security Software

Large Cap GovTech Software

Small Mid-Tech Mid-Cap

Precedent Transactions