2022 Dual Use Report

Discover the latest trends in Dual-Use technology industry analysis and insights into the effects of macroeconomic changes and legislation.

by Benjamin McCrossan, Pablo Rivera, and Sherman Williams

Overview

Welcome to the third annual review of the Dual-Use (DU) Technology industry analysis, where we maintain and update our existing database of DU companies that have raised over $5 million of Venture Capital. We aim to gain insights into trends within the DU landscape by actively monitoring companies within the space.

Background

Venture Capital in 2022 looked vastly different than in the previous two years. Multiple volatile events, with the most significant being rapidly rising interest rates designed to fight inflation, resulted in a rapid increase in the cost of capital. High-growth companies, both public and private, saw significant reductions in their valuations. Venture Capital investment and deal flow also slowed. Lastly, Venture Capital fundraising also slowed significantly as institutional investors looked to shift their portfolios toward more conservative asset classes.

Despite the negative macro outlook, several major pieces of legislation positively impacted the DU landscape in 2022: i) The Infrastructure Investment and Jobs Act, introduced in late 2021, ii) The Inflation Reduction Act, and iii) The CHIPS and Science Act (both introduced in August 2022). All of these bills have significant amounts of money dedicated to industries that fall under the umbrella of DU. However, the most notable impact is on the CleanTech industry, as several hundred billion dollars are dedicated to climate and sustainability-related initiatives.

Lastly, the ongoing conflict in Ukraine and rising tensions with China have significant implications for the DU Tech industry. From supply chains to domestic manufacturing and energy production, the U.S. and its allies must expand the scope of what DU means and invest in these sectors to ensure the ability to compete against potential adversaries.

Methodology

This year's report analyzes 164 DU companies that have raised $5 Million or more in 2022. Our data was pulled from a Crunchbase search and then manually filtered to remove companies that did not meet our criteria. We then used PitchBook, Linkedin, and company websites to fill in additional data.

For our 2022 database update, we continue to use previous metrics of looking only at US and Europe-based DU companies founded after 2000 that have raised over $5 million of venture capital. Notably, this year's methodology differs from the previous reports in one major way. We have filtered the database search to companies that have received some type of government funding. We recognize the differences this may display in year-over-year data sets. However, we believe that this requirement helps identify which technologies the government is actively working to develop. We believe this filter also helps narrow the list of companies to those with direct government use cases versus companies that may eventually have government organizations as customers. We define DU companies as technology-based companies with direct government and civilian applications. This definition excludes companies that may someday sell to the government but do not have specific government offerings as of today. It also excludes service-based companies or companies without technological components. We have also broadened our definition of government to include utilities to better represent government investment in sustainability and infrastructure.

Key Findings

- California, particularly the Bay Area, still dominates the DU Startup landscape. However, 2022 data indicates that funding is more evenly dispersed throughout the country. Massachusetts and Colorado represented the most significant year-over-year increases in funding activity.

- Funding activity for hardware-based firms is on the rise. 2022 saw a massive increase in funding towards CleanTech and manufacturing. This coincides with national efforts to advance these industries.

- Founding team characteristics remain relatively consistent. The average age and previous employers of founders, as well as the number of founders, show little change compared to prior years.

- Diversity decreased substantially in 2022. For example, the percentage of companies with women or minorities on the founding team decreased by nearly 20% from 2021.

- A larger percentage of companies funded in 2022 went through accelerator programs than in previous years.

HQ Location

SF 2021 exceeding the 2000-2020 numbers is likely due to the excessive VC environment in 2021 relative to prior years and relative to today, where we are beginning to see mean reversion with respect to venture investment.

Small changes in the geographic distribution of funding for DU companies have occurred over the past two years. The same states and regions continue to dominate the funding landscape. Northern California, Boston, New York, and Texas all continue to host the largest share of DU companies receiving funding. Notably, however, we can observe a gradual shift away from the concentration of companies in the Bay Area. This shift has moved towards the East Coast, where the total number of DU companies funded in the North East exceeded that of Northern California for the first time. Massachusetts and Colorado had significantly more DU companies funded in 2022 than in previous years.

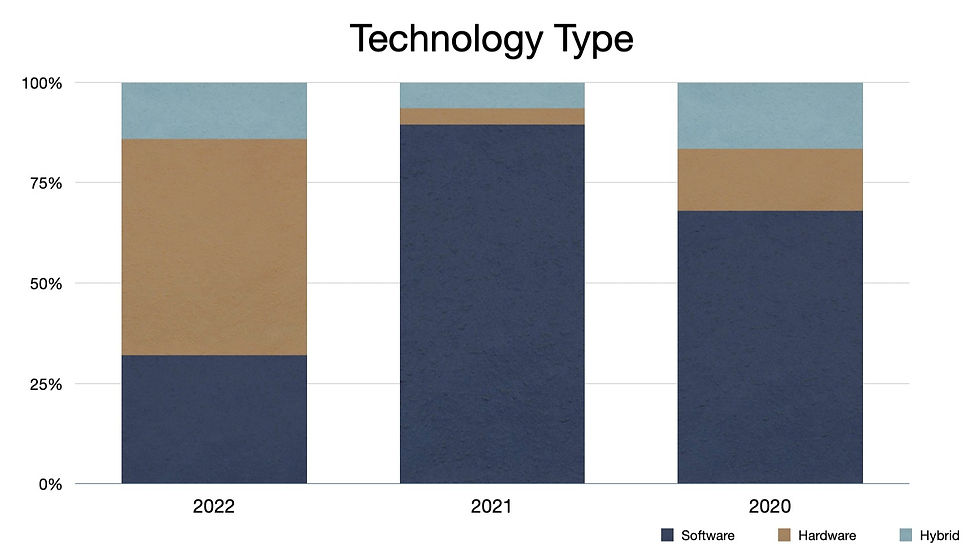

Industry

The drastic shift from software to hardware seen in 2021 to 2022 can be attributed in no small part to a change in our methodology. This change also accounts for the changes in industries funded. Despite these changes, one standout is the rise in government funding for CleanTech and manufacturing. Though the majority of funding is going to hardware, artificial intelligence and cybersecurity also continue to represent a large number of the types of DU companies receiving funding.

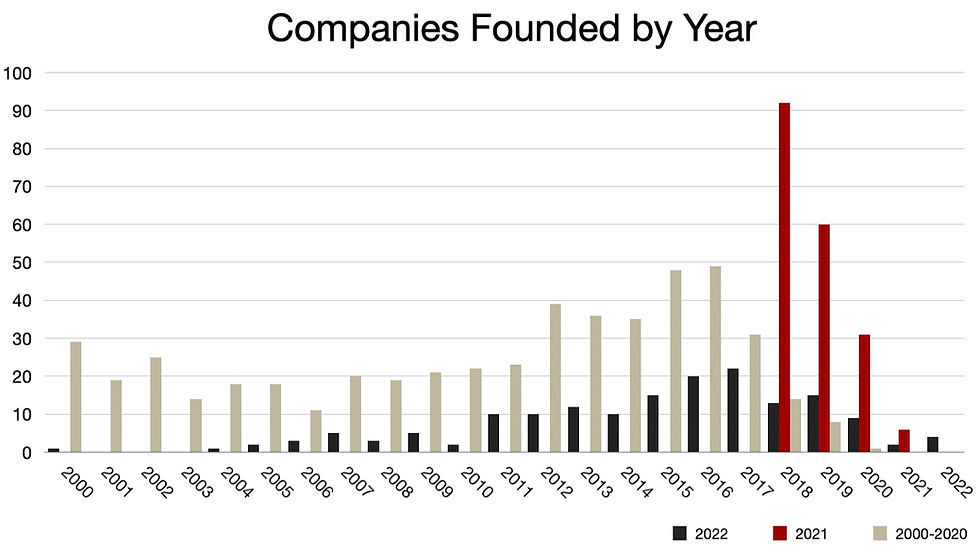

Founding Year

The number of funded DU companies founded tapers off in more recent years. We recognize this pattern across all years analyzed and believe this represents the time required for these companies to mature enough to meet our database's $5 Million funding threshold. We believe that the earlier average founding dates between our 2021 and 2022 companies may be related to the distribution of hardware and software-based companies. One plausible explanation could be that hardware companies take longer to mature and receive significant venture funding.

Number of Founders

The number of companies with 1, 2, or 3 founders is relatively even among the companies analyzed in 2022. This differs with the spike at two founders seen in previous years.

Founder's Age

The distribution of the founder's ages at the time of founding their companies remains relatively consistent with previous years. For example, the mean age of founders for companies assessed in 2022 is 37.3, very close to the database average of 37.9.

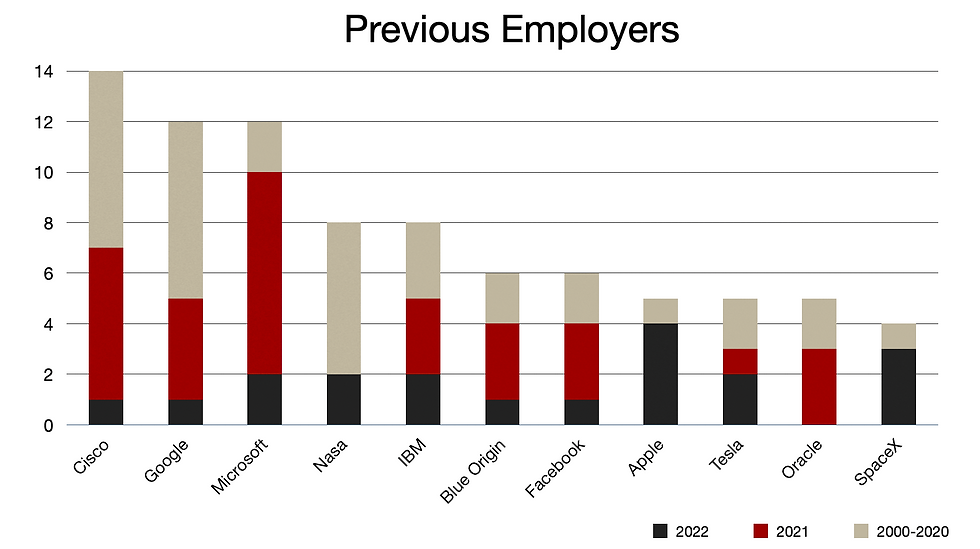

Previous Employers

The founders of companies funded in 2022 have worked at many of the same companies as founders from previous years. The only notable changes in 2022 were the increased number of founders with experience at Apple and SpaceX.

Founder Government Experience

In 2022 we noticed that the percentage of founders with government experience is relatively consistent with previous years. In 2022, 7.3% of founders had government experience similar to our database average from previous years of 7.6%.

Diversity

The overall 2022 data illustrates that diversity rates among founding teams decreased significantly in the last year, declining from 57.7% to 38.2%. In 2022 there seemed to be mean reversion toward the rate of minority founders funded between 2000-2020. Asian founders remained the best-represented minority group in the DU space in 2022. Significantly fewer DU companies with Asian or Black founders were funded in 2022 compared with 2021, while the percentage of Hispanic and women founders remained relatively constant.

Schools

Although undergraduate Bachelors appear to remain uncorrelated in the DU space, Stanford continued to lead in 2022, but it is in a three-way tie with the University of Texas and Ecole Polytechnique. Stanford remains in the lead of DU companies funded between 2000-2022. US colleges dominated International schools in 2022, as 9 of the top 10 are in the US.

Stanford continues to lead the way as the top graduate degree institution in the DU space in 2022. Oxford made a significant jump in 2022, representing the only international school in the Top 25%.

After falling behind MSc for the last two years, 2022 saw a significant increase in the number of PhDs in the DU space. Although the data set depends on company reporting, the increase in academics among the sample size indicates more PhDs entering the DU space in 2022. We believe that this is correlated with the fact that more hardware startups are being funded in the DU space.

BS remains the most dominant Bachelor's degree in the DU Space. BS lead remains above 80% for 2022.

Investors

BPI France was the most active firm in the DU space in 2022. Alumni Ventures, In-Q-Tel, and Khosla Ventures remain among the top investors in the DU space. Notably, many of the most active funds from 2021 are absent from this list in 2022, including Insight Ventures, Lightspeed Venture Partners, Sequoia Capital, and GV. We believe that this change reflects the growing importance of climate/sustainability tech investments.

In 2022, we can see that a larger number of DU companies went through accelerator programs. MassChallenge is the best-represented accelerator amongst our 2022 cohort. This aligns with the uptick in DU funding activity seen in Boston. CDL and Venture Kick are new members to this list. Y Combinator and Techstars remain well represented in 2022 as they have in prior years.

On the Horizon for 2023 and Early 2024

The DU space will continue to grow, catalyzed by open warfare in Europe and sustained geopolitical tension with China. The U.S. government has fully realized that neither the government nor the commercial sector alone can produce the kinds of technologies that will enable the U.S. to maintain technological dominance over time. The U.S. Government must "shape the environment" by incentivizing the private sector to produce certain technologies. The passage of the Inflation Reduction Act and the Chips and Science Act in 2022 represent actions the U.S. government will likely take going forward. While the macroeconomic and macro VC environments will likely be volatile for the foreseeable future, the DU ecosystem is a "bright spot" in the world of venture. It will likely be in growth mode for many years due to the aforementioned catalysts.

A Chat-GPT check informed us that the first use of the term Dual-Use was in 1963 by the Department of Defense. For the last 60 years, that term was largely the domain of the DoD. Competition with China has caused that definition to expand. Areas such as Sustainability (which include climate and energy), several facets of Healthcare, supply chain, and logistics are now firmly represented under the DU umbrella due to their significance to national security. The fact that Breakthrough Energy Ventures is one of the most frequent investors in this year's cohort is a testament to the expansion of the DU term beyond pure Defense/warfighting considerations. AIN Ventures believes that this trend will continue considering access to resources, energy independence, domestic manufacturing, and general technological capability are all security issues. There are outstanding investment opportunities within this expanded DU ecosystem, but a firm understanding of the space is necessary to succeed. We hope our work assists investors and companies as they pursue opportunities within this market.