2022 TACFI & STRATFI Dual-Use Technology Analysis

Analysis of dual-use companies funded through TACFI and STRATFI programs to identify trends and any patterns that correlate with success.

By Benjamin McCrossan, Richard Tippitt, Marta Young

Introduction

AIN Ventures aims to be a leader within the dual-use technology space through diligent monitoring, analysis, reporting, and participation in the investment landscape.

Background

AFWERX introduced the Tactical Funding Increase (TACFI) and Strategic Funding Increase (STRATFI) programs in 2018. The purpose of TACFI/STRATFI (T&S) is to catalyze relationships between Air Force and Space Force end-users and acquisition professionals, private-sector innovators, and investors. The T&S programs bridge the capability gap between current Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) Phase II efforts and Phase III scaling efforts. The programs facilitate the delivery of strategic capabilities for the Department of the Air Force (DAF).

The TACFI program funding ranges from $375,000-$1,800,000, and the STRATFI program ranges from $3,000,000-$15,000,000. Both T&S programs require private funding to match the government funding on a 1:1 ratio. For sake of clarity, this means that all of the STRATFI companies will qualify for the broader Dual-Use technology database that has a threshold of $5M in venture funding raised; however, the TACFI companies may not be represented in the larger database.

We believe these programs help bring innovative commercial technologies into the DAF. The companies funded by the T&S programs represent technologies that the DAF has identified and wants to survive. However, the DAF does not want these technologies to be solely supported by the government. The DAF is helping ensure the survivability of the technology it believes it needs while simultaneously working with the private sector to help these companies become programs of record and bring these technologies into the DoD.

Overview

In this report, we are analyzing the dual-use companies that received funding through the TACFI and STRATFI programs. The purpose is to identify trends among the companies that received funding and compare these trends against our broader Dual-Use database to gain a better understanding of the dual-use technology company set and identify any patterns that correlate with success.

2022 Dual-Use Methodology

AIN compiled a database of Dual-Use (DU) companies, analyzing roughly 688 US and Europe-based companies that have raised over $5M of venture capital in the last 21 years.

We note that the term dual-use is now broadening to include government uses like sustainability and healthcare. It can be difficult to draw a definitive line between what is dual-use and what is not due to this broadening definition, including the fact that companies can eventually become dual-use over time or start off as dual-use and move away from that categorization over time. Despite this, we believe our sample size is large enough to provide valuable insights into this unique set of companies.

2022 TACFI & STRATFI Methodology

In this paper, we are analyzing the 105 Dual-Use companies that have received funding through the SBIR Phase II and follow-on funding from AFWERX's T&S programs. We then created a database using information found on Crunchbase and Pitchbook, LinkedIn, and company websites.

Key Findings

- The companies receiving funding from the T&S programs are concentrated in technology centers like San Francisco, New York, and Austin. However, compared to the broader DU database, the T&S companies are much more evenly spread out across the country.

- Hardware-based companies represent twice as large a share of T&S-funded companies as of DU companies. However, a majority of the companies receiving T&S funding are software based.

- Nearly half of the T&S-funded companies are started by individual founders.

- Founders of T&S companies are generally between the ages of 25 and 35 and are, on average younger than founders of DU companies.

- Only a small fraction of companies have founders with previous government experience.

- Founders of T&S companies have more technical academic backgrounds than founders of DU companies.

- There is little investment from the largest VC firms in T&S-funded companies thus far.

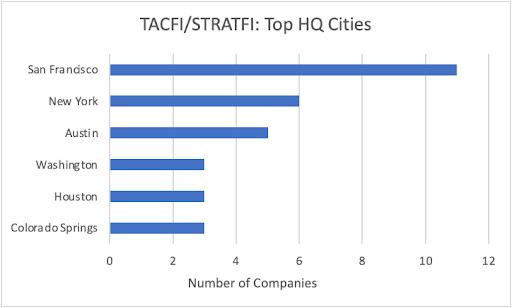

Headquarters Locations

The T&S data indicates that the Bay Area, New York, and Austin represent the greatest number of company headquarters. The concentration of companies in the Bay Area is significantly lower among the T&S companies than the general DU companies. Texas, Virginia, Colorado, and Ohio are all significantly better represented in the T&S database than in the broader DU database. Notably, Seattle, Denver, and Los Angeles are headquarters to relatively few T&S companies, though they are home to many DU companies. The T&S funding is altogether well distributed across the US and significantly less concentrated on the West Coast compared to the broader DU space.

AIN Perspective: The difference in geographies between the T&S and DU companies could be attributed to the difference in industries that are receiving the funding. Texas and Virginia both have an established aerospace presence, which makes sense, considering this is an Air Force-centric database. Colorado has a significant Air Force presence, and Ohio is home to a large manufacturing industry. The funding going to the DMV area could be tied to the proximity of the government agencies. The regional distribution of funding could represent a more balanced approach to the T&S funding compared to regional biases in VC funding.

Key Industries

Cybersecurity and Artificial Intelligence focused companies received the greatest amounts of T&S funding. However, if we combine the wider aerospace industry, including drone, air, and space segments, we see that aerospace companies represent roughly one-fifth of the companies receiving funding from the T&S programs. Manufacturing, microprocessors, healthcare, and augmented/virtual reality companies all received significant amounts of funding as well.

Like in the T&S database, cybersecurity and artificial intelligence are the best-represented industries in the broader DU database. Significantly more hardware-focused companies received funding through the T&S programs than in the broader DU space. Similarly, "hard-tech" industries like aerospace, manufacturing, and microprocessors are much more prominent among the T&S companies.

AIN Perspective: This difference indicates an increased level of funding for "hard-tech" coming from the government compared to venture capital. This reflects the military's need for hard technologies and reflects a preference in the VC industry for software. The focus on aerospace companies makes sense, considering that the T&S program is owned by the DAF.

Company and Founder Data

A majority of both T&S and DU companies were founded in the last 8 years. The number of T&S and DU companies founded tapers off in more recent years. We believe this reflects the time required for these companies to mature enough to meet the thresholds for our databases and does not reflect a slowdown in the space. The general DU database shows an abnormal spike for 2018.

AIN Perspective: The prevalence of companies founded within the last 8 years indicates that the DU space is becoming increasingly dominated by startups vice legacy companies. It also could reflect recent progress made in the startup ecosystem that has allowed DU startups to flourish.

Nearly half of T&S companies are started by single founders. A significantly greater percentage of T&S companies are founded by individual founders than DU companies. T&S companies also have fewer founders on average than broader DU companies.

The most common age range of T&S founders is mid 20's to mid 30's. The T&S founders are on average younger when they start their companies than the DU founders. A majority of DU founders are in their 30's.

AIN Perspective: This seems counterintuitive considering industries like aerospace generally have an older workforce than industries like software.

Neither the T&S nor DU datasets indicate a strong correlation with the founders possessing government/military experience. With that being said, a significantly larger percentage of T&S companies have a founder with military/government experience. USAF veterans are the most represented government entity within the T&S database.

AIN Perspective: We find it fascinating that there is little correlation with respect to the founders having military/government experience. We do want to point out, and this is anecdotal, that while the founders of these companies may not have military/government experience, they often staff their firms with a great deal of people that do.

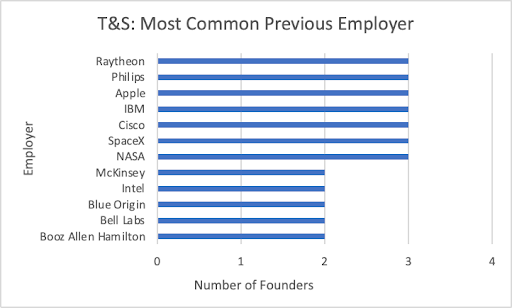

Both the T&S and the DU have strong representation from legacy electronic and computer companies as well as aerospace companies. The broader DU companies also prominently feature more modern software-based tech companies like Google, Uber, and Microsoft.

AIN Perspective: The prevalence of founders, within our T&S database, with experience at legacy aviation firms clearly correlates to the amount of T&S funding going to the aviation industry. The lack of T&S founders with experience at prominent software-based tech companies is surprising considering that a majority of T&S companies are software based.

Diversity

Note 1: The data for all VC-backed companies were pulled from a report published by RateMyInvestor analyzing roughly 10,000 founders of VC-funded companies.

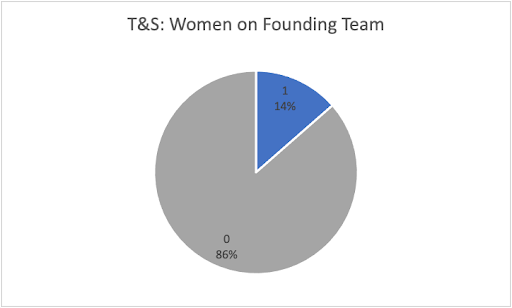

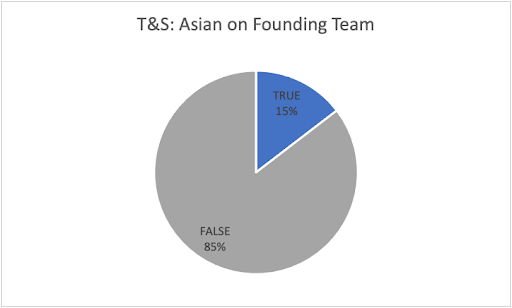

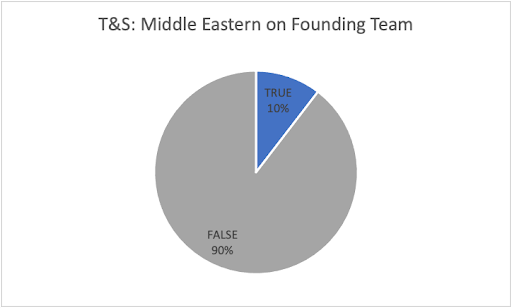

Less than half of the T&S-funded companies have any diversity. The Middle Eastern minority group includes a large number of Israeli founders. Overall, the T&S companies have slightly less diversity than the broader DU companies or the general VC-backed startup space. They also have a significantly lower percentage of Asian founders. The overall diversity of T&S and DU companies is comparable to that of the broader VC-backed startup space.

AIN Perspective: The number of Israeli founders seems reasonable considering the strength of Israel's aerospace and defense industry. The lack of Asian representation among founders of T&S companies could be partially attributed to geographies and industries as the West Coast represents a smaller percentage of T&S companies, and software also represents a smaller fraction of T&S companies.

Degrees

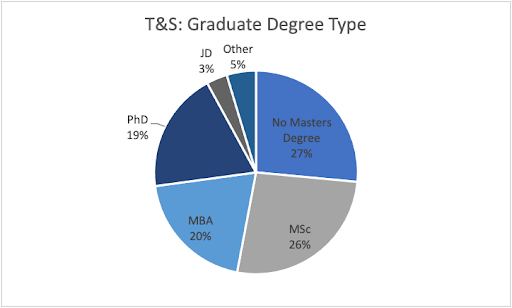

A majority of T&S founders have BS undergraduate degrees. A majority of T&S founders also have graduate degrees as well. MSc's are the most common, representing roughly 20%, followed by MBA's and PhD's, which both account for roughly 20% of founders.

A larger percentage of T&S founders have Bachelor of Science undergraduate degrees and graduate degrees than DU founders. PhDs are also twice as common among T&S founders as they are among DU founders.

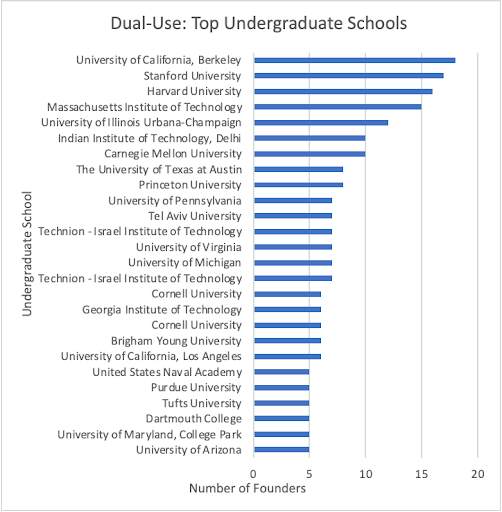

For undergraduate institutions, schools with strong engineering programs are particularly well represented. Liberal arts schools have little to no representation among these founders, and there are no Ivy League schools home to more than two founders on this list. Brigham Young also makes a strong appearance on this list. There is very little representation of schools outside the US among T&S founders. The graduate schools show a stronger bias towards the usual prestigious institutions and less towards engineering schools.

The broader DU database represents far more institutions outside the US, particularly from Israel and India. It also shows a strong bias for schools with top engineering programs, but less so than the T&S database. Traditionally prestigious schools are also much better represented than in the T&S list.

AIN Perspective: The prevalence of engineering schools and advanced degrees among founders of T&S companies indicate a deeper technological focus in T&S-funded companies compared to the broad DU space.

Investor Data

To analyze the investors of each company, we included only the 6 largest investors in each. For the T&S companies, In-Q-Tel and Alumni Ventures were the most prominent investors. TechStars was the best-represented accelerator by a significant margin. These companies, as a whole, lack backing from the biggest names in VC.

AIN Perspective: This could indicate the geographic distribution of the companies — in locations other than Northern California. It could also be a result of the industry focus, as many of the bigger VC firms focus on software. It could also be a result of the fact that the majority of companies in the T&S database are actually TACFI companies, and they may be too small (early in their development) to warrant much interest from larger firms.

The largest VC firms are the best represented on this list, demonstrating that DU companies are able to attract blue-chip investors. The biggest incubators are also well represented on this list, proving that traditional incubators are quite effective at launching DU companies.

Conclusion

The Dual-Use technology landscape is expanding rapidly, and we at AIN Ventures believe the catalyst is the great power competition between the U.S., China, and to a lesser degree — Russia. These countries are now competing in every aspect of the technological and defense landscape. Evidence of this fact is the bi-partisan passage of bills that are meant to maintain U.S. technological advantage and recent moves by the Biden administration to limit U.S. information sharing with China's technological industries.

Programs like TACFI/STRATFI are essential to ensure the military has access to top-tier technology, which is important considering technological advancements are often borne outside the military. It is still to be seen if the matching funding of the T&S program is enough of an incentive to ensure the government is getting access to the best technology and that this program helps to ensure the survivability of these companies. Further, a key element of the SBIR program is to ensure companies eventually matriculate to becoming programs of record, and the verdict is still out on this coming to fruition.